Suddenly broke: Financial advice for sports millionaires

January 11, 2023

Click here for the original DER SPIEGEL Article

When Greg Oden talks about how he used to waste his money, the former professional basketball player remembers the trunk of his first sports car. He had treated himself to the car in 2007 after he

made it into the NBA and signed a four-year contract worth around $22 million.

Oden, who was 19 years old at the time and was seen as a future superstar, went straight for it: a Dodge Charger, red body, tinted windows, rear spoiler, a television in the dashboard, a high- end music system. And: »I had loudspeakers installed in the trunk, which I could turn out at the push of a button«, says Oden, now 34, »under the tailgate there was a logo with my initials.« The interior alone cost around 60,000 dollars .

About ten years later, Oden’s account was largely empty. It didn’t stop at the extravagant sled. Oden had bought houses, supported friends and relatives, bought more cars – until there was hardly anything left of his wealth. He himself hadn’t noticed anything about it: »I simply didn’t know my account balance.« He trusted that his financial advisors had everything under control. It was only when he realized by accident in 2018 that he could probably slide into bankruptcy within a few years if he didn’t immediately curb his expenses, did Oden decide to change his lifestyle.

Many athletes are denied this late insight. Some world stars who take to the field like superheroes

who are celebrated, privately fail to keep their breathtaking fortune together. It even hits the biggest: Boris Becker, Mike Tyson and Diego Maradona blew away amounts that should actually last a dozen lives in just a few years. Tyson alone is said to be around

$400 million in fees and advertising revenue, but the money didn’t even last until the end of his career. Others, like tennis veteran Becker, even have to go to prison at times because they try to avert or cover up the ruin in a criminal way.

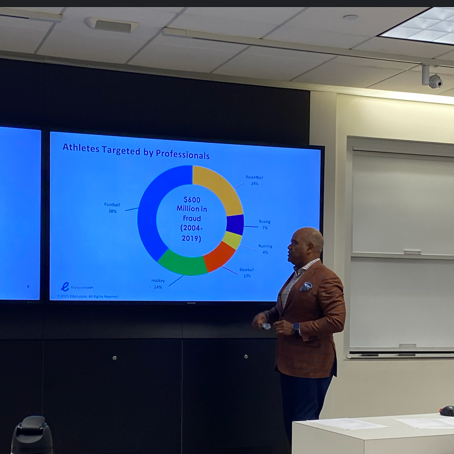

The bankruptcy virus is particularly rampant in US sports. A working paper from the National Bureau of Economic Research states that about one in six American football NFL professional runs out of money within 12 years of retiring. A long career and a good income “doesn’t offer much protection against the risk of bankruptcy,” write the Cambridge research team. Other sources describe the situation even more dramatically: almost 80 percent of all NFL professionals would go bankrupt when they retire, and the figure for NBA basketball players is around 60 percent.

Why is that?

Drew Hawkins can talk for hours on that question alone. The American, 55, worked as a manager at the investment giant Morgan Stanley. He has been advising professional athletes on their investments for almost three decades – and according to his own information, he has “the good, the bad and the ugly sides of some of the biggest names in entertainment«. The problem with athletes who can’t keep their money together is “really, really bad,” says Hawkins. A key problem is that many young millionaires don’t give a damn about their finances during their sporting careers, under the mistaken belief that the plentiful flow of money will go on forever. But on average, an NBA career lasts less than five years, and in the NFL it washes players out of the league after just over three seasons. Then many lack a plan B and the willingness to curb spending.

Hawkins still remembers his first conversation with a multimillionaire NFL professional. That was in 1994. The conversation with him

Athletes, whose names he was not allowed to name for reasons of discretion, were new territory for him. “I asked him simple questions: Who pays your bills? Who has access to your accounts? Do you have a monthly budget?” Hawkins lists it, “but he just sat back in his chair and always had the same answer: I don’t know, you’ll have to ask my agent about that.” After a short time, he found that too stupid become. “I just told him: The arrogant way you’re answering me doesn’t bode well for your future.”

Especially at the beginning of their career, many young millionaires want to flaunt their new wealth – or feel compelled to do so. He was struck by the idea of keeping up with his teammates, “with the flashy cars and the jewels,” Terrell put it Owens, 49, Owens, 49, once, former star player in the NFL. These are “the most idiotic purchases a player can make, especially if you don’t have the money.” Owens himself earned around $80 million as a professional and spent almost everything again.

There are grotesque stories about gamblers and how they deal with money. Former NBA pro Gilbert Arenas, who once owned around 500 firearms, had a shark tank installed in his $3.5 million mansion, which costs around $80,000 a year to maintain. Vince Young, once an NFL quarterback, is said to have bought all 120 tickets for a scheduled flight from Nashville to Houston so that he could have peace of mind on the flight. Golf pro John Daly gambled away $1.65 million in one day in Las Vegas.

The shortcomings of the American educational system are evident in the athletes, he says Investment Advisor Hawkins. “You can finish your finance studies at Harvard at the top of your class and still have no idea how a loan works.” He himself went to a private high school and a prestigious college, in addition to teaching for lack of alternatives – ven only took courses in home economics and wood processing. “I could make an awesome grilled cheese sandwich or carve you something out of wood, but I didn’t know anything about money.”

Most of America’s basketball, football, and baseball talent finds its way into pro sports without a college degree. Some are still teenagers when they are presented with their first contract, which makes them millionaires overnight. In the NBA, for example, the average salary is currently more than $8.2 million per year. “We’re usually talking about young men from poorer backgrounds here,” says Hawkins. “Imagine you’re 19, 20 years old, you come into the NBA and you have to prove yourself at the highest level while at the same time millions are pouring into your bank account, but neither you nor your family have a plan on how to deal with it .« That is the moment when many players come across so-called scammers: advisors who supposedly mean well – and who often rob the players of their assets.

In April, a former employee of the former NBA proand today’s TV commentator Richard Jefferson was sentenced to nearly six years in prison. As a personal assistant, he forged the athlete’s signature to open an account in his name, which Jefferson was initially unaware of. The man then diverted a total of around seven million dollars into his account over a period of several years, making a fine living with it: he wanted to buy luxury cars, vacations and even a plane with the stolen money. It wasn’t until years later that he broke. “It starts out at $500 to see if the player notices,” says financial expert Hawkins, “and then the amounts steadily increase. At some point you wake up and realize you’re short of $20 million. Or 100 million.« In 2018, Olympic basketball champion Kevin Garnett sued his former agent, who allegedly stole him $77 million. The manager was already in jail after confessing to stealing millions of dollars from another high-profile client, five-time NBA champion Tim Duncan.

It’s not just strangers who want the athletes’ money. Especially with athletes who have made it out of poverty, friends and relatives often hold out their hands and demand their share of the gain. That’s how it was with Greg Oden, the basketball player with the decadent trunk. “I left mine

my cousin live with me, my best friend, my uncle,« says Oden about his early years in the NBA, which he spent with a team in Oregon, around 3000 kilometers from his parents’ house. He also made sure that his brother received money every month, his father, his mother, his grandmother. For other family members, he set up a pot from which they could help themselves when they were short on cash. “The only problem was: the pot was quickly empty, the relatives kept coming back,” says Oden.

It’s okay to support people, says expert Hawkins, as long as you set limits. “I always ask the players: how many families do you know where the parents say, great, Joe got a well-paying job at IBM, so I can stop working now and let him put me through? « The answer is always: not a single one. It’s different in professional sports.

Many do not want to hear such advice. Antoine Walker, 46, was one of them. The former basketball pro received around 110 million dollars, but back in 2010, only

two years after his last NBA game, he had to file for bankruptcy. His entourage alone, for which he bought houses and financed their lives, cost him around 36 million dollars. He lost another $20 million on failed real estate investments.

Vin Baker, now 51, also fell deeply. In 1993, the son of a car mechanic came as

highly traded talent in the NBA, was meanwhile one of the best players in the world. Away from the court, the Olympic champion squandered his fortune in strip clubs and casinos. He once lost around a million dollars in a single night playing blackjack in Las Vegas. Added to this were Baker’s addictions: first marijuana, later pills, especially alcohol.

Baker became so addicted that he filled a plastic drinking bottle with rum and secretly sipped it during ongoing games. He got caught, changed teams, got more chances but didn’t manage to stay dry. It wasn’t until 2011, after his fifth therapy, that he got off the bottle permanently and was able to start a new life – without the approximately 97 million dollars he had earned in salary during his career. He had spent everything.

“Money hasn’t changed me as a person,” Baker wrote in his autobiography. It merely reinforced his “bad character traits” that he had developed through the alcohol.

Learning effects from scandal stories like that of Baker and Walker are apparently small. Two years ago, American ice hockey pro Evander Kane, 31, filed for bankruptcy. The striker, whose earnings had totaled around $50 million by then, had accumulated a mountain of debt of around $27 million. He is addicted to gambling, said Kane, who is still active in the professional NHL league.

“I’m scared of credit.”

A player in the United States Basketball League

If the correct account is empty again and the need is great, some drift into crime: In 2021, the FBI set up a fraud ring involving 18 former NBA players. Using fake medical bills, the athletes siphoned off several million dollars from a health fund that the league has set aside for former players. The head of the gang, who previously earned around seven million dollars in the NBA, is now facing up to ten years in prison.

How can such tragedies be prevented?

»You have to take the young people by the hand«, says Drew Hawkins, on a sunny July day in Washington, D.C. He is standing in a gray conference room next to a basketball hall, a projector is projecting a slide onto the wall: »Money Mind«. Ten of the best basketball players in the world enter the room in slippers and shorts and fall into heavy armchairs, it is the Washington Mystics team from the US women’s league WNBA. Hip-hop music can be heard coming from the speakers: the song is called “Whole lotta money”, quite a lot of money. Hawkins takes a seat in the back row and nods to an employee, the signal to start.

In 2018, Hawkins founded Edyoucore, which has been offering seminars for professional athletes and artists ever since. In the sessions, he teaches the basics of financial literacy: How do I find the right advisor? How do I make a financial plan? What percentage of my earnings should I save? He now works with over a dozen NBA teams, and he also has partners in the NFL. The teams bear the costs.

»We don’t want to sell you anything«, Hawkins’ employee opens the workshop in Washington, »none of us want your money.« Next to the seminar leader is Rushia Brown, herself a former WNBA player who is now an athlete in the transition from the sport – accompanied in the further professional career. She tells of a teammate who became homeless after her career and of a consultant who cheated her out of money. “You have to do your homework and check who you’re bringing into your team,” she says.

“I’m scared of credit cards,” says one player. »What worries and fears do you still have?« asks the lecturer. “That I’m alone now, but want to take care of a family later and need money for that,” says another player.

Women tend to be more likely to keep their money together than men, Rushia Brown said after the meeting. “That’s also because they don’t earn that much.” The average salary in the WNBA is around $100,000, about a fiftieth of what men in the NBA earn on average. “The ladies know that they’re after still have to work on their basketball career.

- Like